India at a Crossroads

India’s automotive story is entering a new epoch. For decades, mobility was about affordable hatchbacks diesel–petrol debates and the dominance of Maruti and Hyundai. By 2025 the country finds itself on the cusp of a silent revolution. The hum of electric motors once rare now echoes across Delhi Ring Road, Pune IT corridors and Bengaluru startup campuses.

But how real is this transition? Beyond media buzz and corporate announcements the truth lies in government data, hard sales numbers and the lived reality of infrastructure. Let us dissect India’s EV pivot through the lens of numbers and narratives.

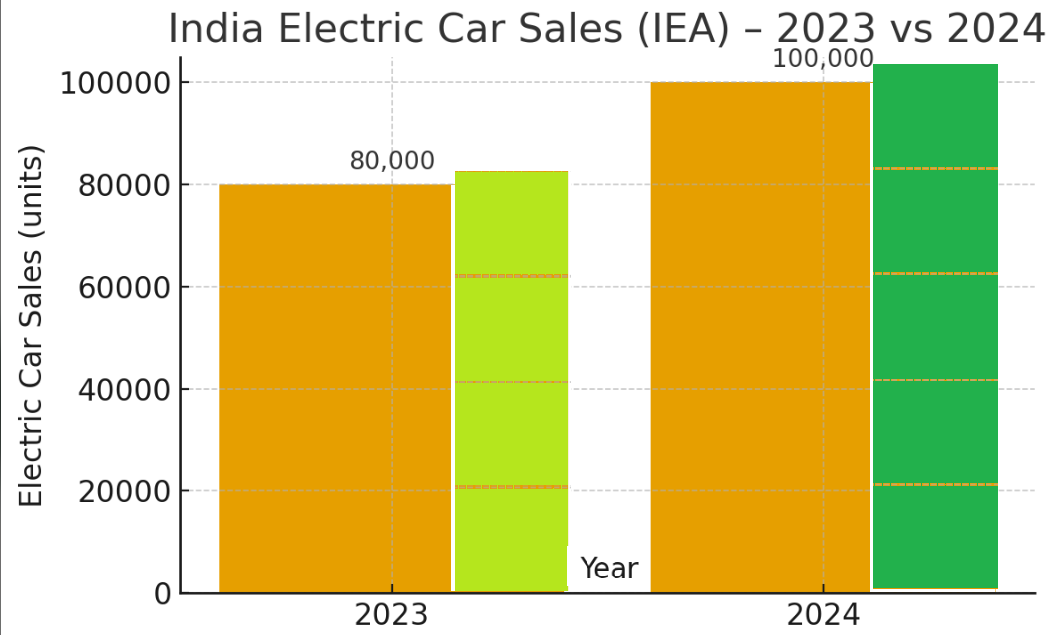

Sales- The Long Road to Scale

According to the IEA Global EV Outlook 2025 India’s electric car sales in 2024 touched ~100,000 units up from ~80,000 in 2023. This represents about 2% of all new car sales modest compared to Europe~25% or China~38% but significant for India’s nascent market.

Why does 2% matter? Because India is a price-sensitive market where even small shifts signal structural change. An Indian family buying an EV today isn’t just chasing technology it is making a financial gamble on fuel savings, maintenance cuts and resale value. Each of these ~100,000 sales represents not just a car but a vote of confidence in the future of electric mobility.

Infrastructure- 16x Growth in Just Over Two Years

Sales alone mean little without infrastructure. Here India progress is striking.

- March 2022– 1,633 public EV charging stations

- Dec 2022– 5,151

- Dec 2023– 11,903

- Dec 2024– 25,202

- April 2025– 26,367

In just over two years chargers multiplied 16 times. That growth trajectory is faster than even India’s telecom revolution in its early years.

Chargers remain clustered in metros and highways leaving Tier-2 towns anxious. The real test will be whether Kanpur, Jaipur or Patna drivers can trust the charging grid as much as Delhi or Bengaluru residents do.

State-Wise Leaders- A Tale of Unequal Adoption

EV adoption in India mirrors its economic geography.

As of April 2025, the top 10 states for public charging were:

- Karnataka- 5,880

- Maharashtra- 3,746

- Uttar Pradesh- 2,137

- Delhi- 1,951

- Tamil Nadu- 1,524

- Kerala- 1,288

- Rajasthan- 1,250

- Madhya Pradesh- 1,054

- Gujarat- 1,008

- Telangana- 976

Karnataka leads thanks to Bengaluru tech ecosystem and proactive state policies. Maharashtra follows with Mumbai–Pune corridor investments. Delhi stands out not for absolute numbers but for density chargers per sq km are higher than any large state. Uttar Pradesh surprises many by making the top three reflecting policy pushes in Lucknow, Noida and Ghaziabad.

The Other India- Underserved Regions

India’s uneven EV geography. Bihar has only 118 chargers, Odisha 230 and Chhattisgarh 244. Together, these three states house over 150 million people but fewer chargers than Delhi alone. Eastern and Central India despite rapid urbanization barely register on the EV map. Without addressing this gap India EV revolution risks being confined to western and southern corridors

The FAME-II Ledger- Where Government Money Went

The FAME-II scheme has been India’s most important EV catalyst. According to government data (MHI- March 2025)

- 16.15 lakh EVs supported across categories.

- 22,548 electric four-wheelers incentivized.

- 5,135 e-buses delivered out of 6,862 sanctioned.

- 9,332 charging stations sanctioned under FAME 8,885 installed by June 2025.

This means about one-third of Indian public charging infrastructure stems directly from FAME-II funding while the rest comes from state schemes, PSUs and private charge point operators.

Challenges remain. Subsidy misuse allegations led to scrutiny delaying disbursals. Some OEMs paused EV plans waiting for clarity on FAME-III. This uncertainty underscores India policy paradox bold announcements often clash with patchy execution.

The Consumer Lens- Price vs Trust

Consider this an entry-level petrol hatchback starts at ₹6Lakh while a comparable EV begins at ₹12lakh. That sticker shock is real. But lifetime economics are shifting –

- Running cost- ~₹1 per km (EV) vs ₹6–8 per km (petrol/diesel)

- Maintenance- 30–40% lower in EVs

- Incentives- road tax waivers in Delhi, Maharashtra and Tamil Nadu

Still, range anxiety, resale uncertainty and limited service centers hold back adoption. The key unlock is domestic battery manufacturing. With PLI schemes driving giga factories localized cells could cut costs by 20–30%. When that happens, India will see its first truly mass-market EV hatchback at ₹8–10lakh a moment that could flip adoption curves overnight.

India Unique Path

Unlike China subsidy-heavy model or Europe climate-driven mandates India EV journey is hybrid. Two- and three-wheelers dominate early adoption accounting for nearly 80% of EV volumes. Cars are catching up slowly led by fleet buyers and metro consumers.

Grid Impact– The Invisible Backbone

Charging infrastructure is only as good as the grid that feeds it. India’s DISCOMs are under stress but reforms are emerging:

- Time-of-Day Tariffs– cheaper night-time charging encourages load balancing.

- Open Access Rules– allow private charging operators to source renewable power directly.

- Integration Challenge– by 2030, if India meets its 375,000 chargers target grid capacity must expand alongside. Otherwise, peak load pressures could derail the EV transition.

EV adoption is therefore not just about cars and chargers, but about grid modernization and renewable integration.

The global lens also matters- India demand will shape global lithium, nickel and cobalt markets while its software-driven startups (telematics, charging apps, fleet optimization) can export solutions globally.

What’s Next? – For 2025–2030

- Sales– India could reach 8–12% EV share in car sales by 2030 if affordable models launch.

- Charging– Govt targets 375,000 public chargers by 2030 nearly 15x current levels.

- Policy– FAME-III clarity and state-level mandates will decide momentum.

- Investment- Battery giga factories, highway corridors and fleet electrification are the hotbeds.

India EV revolution is still embryonic but the momentum is undeniable. Sales are climbing, chargers are multiplying and policies are nudging the market forward. Yet without affordable EV and domestic batteries adoption risks plateauing. The next five years will decide whether India’s electric story becomes a breakthrough or stalls as a half-measure.

For EVCarBazaar readers the signal is clear the quiet hum on India’s roads is about to get louder.